The EU is set up to fail

On the electoral success of Wilders and the PVV in the Netherlands

The election of Geert Wilders in the Netherlands is remarkable, considering how the Dutch see themselves and their liberal heritage. I’m new here so I, apart from being a part of the problem for the PVV voters, can only but give very prelimary impressions of a newcomer.

The day after the election, I listened to a lunchtime TV programme where they asked people why so many voted for Wilders’ PVV. The reaction: the middle classes, despite everybody saying the Netherlands is a rich country, are suffering. Besides migration, they repeatedly mention the soaring cost of living and house prices in particular.

But also the protests against Zwarte Piet and climate activists blocking highways, and the fact that for years, the centre-right Rutte government has been saying it will address these issues, but it hasn't, and it's only gotten worse.

And, of course, migration is blamed for this suffering of the middle classes. The high house prices are a good example of the muddled scapegoating, here too, migrants are said to be responsible, and not the primary culprit, the quantitative easing (QE) in response to the financial crisis that saved the world - and the Dutch - economy from collapse.

QE worked as intended by lowering interest rates and inflating asset prices. The problem is property is a very attractive asset. During Covid, QE was extended, along with other help, and interest rates plummeted further, and house prices grew even faster.

The Netherlands is a rich country

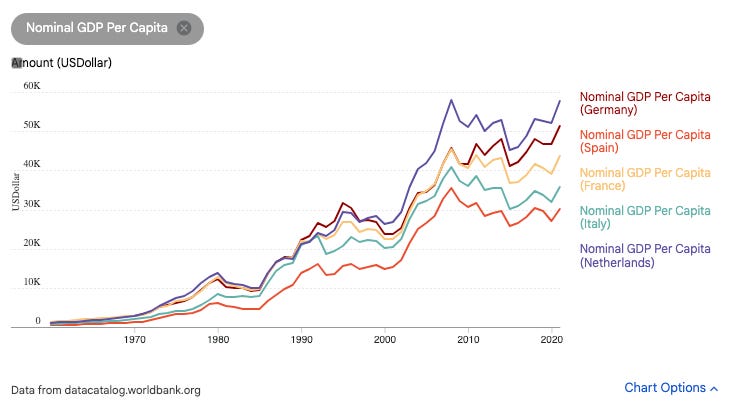

Some context, the Netherlands is indeed a rich country. GDP per capita in 2021 was $11,000 USD higher than in the UK, and it’s about $5,000 higher than Germany too.

And its not as if these riches are not shared. It’s a much more economically equal country than the UK or even Germany, with a Gini coefficient, a measure of income distribution, of around 0.29, which places it among the top 12 globally, with a more equal income distribution than Sweden, Denmark or Finland. A number that has not changed significantly since the early 90s.

However, it should be noted that the devil is again in the details, and Gini is a rough guide. Preliminary data shows top income earners benefitted from the pandemic, relative to the bottom 50%. And that the bottom 50% has been taking about a 4% lower income share when compared to the 1980s. See the graph below.

The population has increased steadily, with no marked increase in the last 20 years. It grew faster in the 1960s and 1970s. And the debt to GDP ratio is a very low 46.7%. The major discontinuity from past trends is that growth since the financial crisis has slowed markedly, not surprising since more than 60% of its trade is with Europe, which suffers from the same problem. However, it has done better than the most developed Western European countries, bar Germany.

So, on the face of it, the crude numbers don’t show the basis for the unhappiness. But looking closer may reveal trends within these numbers that tell us more. So for example, birthrates of the “native” Dutch could be less, and immigrants a bigger percentage of the population even if migration is similar to before. That is indeed what the right here thinks.

Things will only get worse

It is all the more depressing when this rightward shift is plotted against future trends. Climate change is only starting and will add to the pressure the Dutch middle classes are facing. Things will likely get worse, too, on the immigration front, with more pressure likely because of climate change-induced disruption.

The costs of climate change - including lower growth - will pile up the longer it takes to address it aggressively. The AI revolution could massively boost productivity — and, with that, growth, but it also could cause major disruption in labour markets, especially among middle class workers. So don’t bet on AI helping the general sense of unhappiness in the short term, but rather adding to it.

Neither does it help that refined petroleum remains the Netherlands’ main export. The country has a significant stake in the status quo. Its CO2 emissions per capita is significantly higher than France or the UK’s.

Add to that the risks to the open Netherlands economy of geopolitical competition and an ever more fragmented global economy. The Netherlands is a major hub of world trade, the 6th biggest exporter, and the 8th biggest importer. While the Netherlands is not nearly as exposed as Germany with exports to China, who won’t be able to rely on exports for growth as it has in the past, the Netherlands will suffer if the German economy does. Germany is its largest export destination.

If the Dutch turn rightward under these relatively benign conditions, where will they end up in five to ten years’ time? Will they eventually settle on no free movement of people and enforce border controls within the EU? That’s a principle which is held as sacrosanct within the EU. But it surely looks like that is where we are heading.

So you have to wonder how the Dutch will react in the future and whether the European Union will be able to withstand these pressures. If I were a betting person, I would probably say, if the relatively privileged Dutch do not withstand them — then no, the EU won’t either.

The design flaw at the heart of the euro

On the macro-level I have more of a footing for commenting. I've been closely watching events and reading about the structural issues of the European Union for several years. Full disclosure: I advise a major European bank on public policy. I've been reading about monetary and political theory about what makes societies work. All of this points to one conclusion: the EU, as it is currently constituted, must move forward to closer integration or backwards (voluntarily), or it will come undone in a drawn-out, destructive, acrimonious way.

Let's start with the money stuff. As Joseph Stiglitz pointed out, the EU has a problem — the euro. Instead of creating a convergence between its members, the euro is pushing member states apart, and it is also one of the most significant reasons it is not growing faster. This should matter to the Dutch because as I have already pointed out, unlike Germany, the Dutch economy depends much more on trade with Europe.

The belief was that free movement of capital, enabled by the euro, would lead to increased efficiency and, consequently, prosperity. This view saw the euro as a facilitator of capital mobility. However, this overlooked a critical element: the integral role of the state as the ballast of any banking or financial system.

Yet the EU was not conceived as a state, never mind a super-state. So the Euro is effectively stateless money. This is why, when the 2008 crisis hit, which started in the US, capital did not flee the US; it streamed there from the EU. Money managers knew the might of the US state had its banks’ backs.

In Europe, this issue also manifests as follows: Given a choice, investors prefer putting money into the German banking system and state over the Spanish. The Euro and single market make this transfer easier, resulting in capital flight from Spain to Germany, particularly in times of stress. This outflow impacts Spanish banks' ability to lend.

The ideologues behind the euro assumed that a small Spanish business, like a dry cleaner or grocery store, could easily secure loans from large German banks. However, this ignores the local nature of information and relationships in banking. The movement of capital out of Spain, therefore, led to massively reduced lending to local businesses, causing a destructive economic impact.

So the euro area established a system where a negative shock exacerbates problems, prompting capital to flow towards stronger economies and slow growth. This structure essentially means that in times of trouble, resources in the eurozone move away from those who need them most. We saw this with the Russian invasion of Ukraine, how Europe, who was in the process of stopping QE and raising rates to combat inflation, had to announce special measures to support Italy’s ability to finance its debt.

Why was this moment considered dangerous? Because it can set in train the so-called sovereign banking doom loop. The doom loop is a perilous entanglement between a nation's fiscal health and its banking sector. For stability's sake, banks need to hold substantial safe assets, usually government debt. Fiscal distress diminishes these bond values, eroding bank balance sheets. Weakened banks may necessitate government intervention, often as bailouts, further inflating public debt.

This escalation of government debt compounds the crisis, devaluing bonds further and intensifying banks' vulnerabilities. This is what we observed in Greece and Italy. The process can also start with banks, where healthy government balance sheets can be thrown in the red, when saving their banks, as happened in Ireland and Spain.

This scene still haunts Europe today since it still has no banking union like all successful states do. It impacts weaker states’ growth and eventually the Netherlands’ own.

First and foremost, the eurozone needs shared deposit insurance like the US does. As Stiglitz explains, if Washington State had been responsible for bailing out Washington Mutual, one of the US’s largest banks, it would have faced significant difficulties. The state's moderate size and resources would have made such a bailout a formidable problem. However, the rescue did not fall on the state but was handled by the Federal Deposit Insurance Corporation, a federal entity.

Yes, having a banking union would imply that taxpayers in the Netherlands might be needed to help prop up a weaker state, but that is the price one must pay for all the benefits the union has bestowed on the Netherlands, but more importantly, for a flourishing EU economy from which it will benefit. That growth, cheap capital and frictionless trade with the rest of Europe are not the only benefits.

The Netherlands and Germany in particular, have benefited from the euro being a cheaper currency, making their exports more competitive globally. If they had their own currency instead, it would appreciate immediately and reduce exports.

So they should thank Italy, Spain, Portugal and Greece for sharing a currency. If the EU fails over immigration, the euro would also be a goner. I don't think the export-orientated countries in the north have communicated what this would mean to their voters. But even if they did, I still don’t think it will be enough to change minds. And here is why.

The trilemma of integration — (or its identity stupid)

The fundamental problem for the euro and the EU lies in the realm not of the economy but in identity. It is the most critical issue that the market-orientated designers of the euro never anticipated.

Harvard economist Dani Rodrik has posited a trilemma on economic integration: To have economic integration between different countries, one must sacrifice either democracy or sovereignty.

In other words, to maintain democracy, one must vote within that new larger body, such as the EU. This means that the Dutch citizens would vote alongside the Germans, the French, the Italians, thereby relinquishing national sovereignty and vetos. Their national voice would be subsumed by citizens’ individual votes in a larger polity. The Dutch would become Europeans first and foremost like Americans are.

If, instead, one wants to integrate but preserve national sovereignty, one must give up on democracy. This is what the EU has become. You have a situation where citizens in member states want certain things done, and even vote for them, but they are not implemented because of the contradictions inherent between international economic integration and national democracy.

For example: A year before Wilders launched his party, in 2005, first the French and then the Netherlands resoundingly rejected the newly proposed European constitution. Despite these setbacks, EU leaders and subsequent EU Presidency holders were keen to keep the constitutional project alive.

This commitment led to the negotiation of the Treaty of Lisbon, which retained many elements of the Constitution but in a different format and under a new name that was not put to voters. The Treaty of Lisbon was signed in 2007 and came into effect in 2009.

So Wilders has a point about the EU being anti-democratic. There is, of course, another way around this problem. That is to opt for democracy and national sovereignty and give up on the European Union altogether. That will be worse for the Netherlands than the PVV voters imagine but better than the slow train wreck that is the current unhappy marriage.